To comply with Regulation Best Interest and Department of Labor regulations, firm policy requires 401(k) rollovers to be identified as the result of either Education or Recommendation conversations. Please reference prior training on the topic of Education vs. Recommendation available through the Agent Portal: DOL 2.0: Education and Recommendations (mailchi.mp)

As a reminder, Recommendation conversations are not general advice, and involve the Registered Representative making calls to action based on a specific customer’s individualized needs, such as: “I think you should….” or “I recommend you rollover this 401(k) into an IRA”.

In contrast, Education conversations are typically more general and informational in nature. For example, rollover education will discuss the pros and cons associated with moving money to an IRA, versus leaving it in the 401(k) plan or taking a distribution. After providing that information in a neutral fashion, the client ultimately decides whether they’d like to rollover their 401(k) into an IRA without a recommendation. If a rollover occurs, the Registered Representative may then assist in identifying which type of investment product(s) should be used for the IRA, at which time the Registered Representative can make product recommendations.

New Annuities

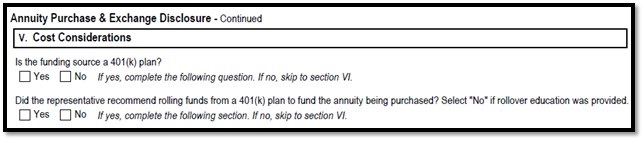

All new Annuity purchases require the Annuity Purchase & Exchange Disclosure (“APED”) form to be completed. The APED was recently enhanced for ease of use on page 5, Section V (Cost Considerations) to assist you with clearly documenting whether the Education or Recommendation process was utilized when the funding involves a 401(k).

If Education was used, you answer “no” to the second question and then proceed to the next section. However, if Recommendation was used then you would answer “yes” and complete the remainder of Section V, including a cost comparison between the 401(k) and Annuity.

Existing Annuities

The APED is only used for new Annuity purchases, while the Source of Funds form is used for additional investments. In addition to the Source of Funds form, you will need to provide either the Defined Contribution Rollover Education or Defined Contribution Rollover Recommendation if a 401(k) is part of the funding. The selection between the two versions, Education or Recommendation, will be based on your conversation with the client.

404(A)(5) – Participant Fee Disclosure

If Recommendation was utilized you will need to complete a cost comparison using the 404(a)(5) – also known as the Participant Fee Disclosure, which is available from the 401(k) provider. If the client is not able to provide you with a copy, then you are able to reference proxy information available through the Agent Portal: 401(k) Plan Data (nationallife.com)

Keep in mind that whenever Recommendation is utilized, the Client Relationship Summary needs to be provided to the client, even on additional investments.

84-24 Qualified Annuity Disclosure

The 84-24 Qualified Annuity Disclosure is required with any qualified Annuity regardless of the funding source. It should be completed at the time of a new purchase, or if you’re recommending adding to an existing annuity and it is not already on file, is no longer effective (the form becomes stale 3 years since last acknowledged by the client), or information on the last disclosure on file has changed (e.g., your ESI payout rate changed).

When the 84-24 requirement first went live and ESI noticed that the form was not on file for existing annuities, we sent reminder emails as a courtesy, however this has been discontinued effective 04/01/2023. Registered Representatives continue to be responsible for ensuring the form is completed and on file when applicable.

Questions

If you have any questions, please contact your supervisor or ESI Direct Business Suitability at 800-344-7437.

TC132996(0423)1