The S&P 500 index was up 9.11% in July, which has some market pundits suggesting that the bear market is over. Conversely, it seems like an equal number of market prognosticators are warning that the July returns were simply a bear market rally, and a lower bottom is yet to come. Was the rally in July a precursor for more positive near-term performance or merely a bear market rally? Have we seen the market bottom? How should clients invest given the uncertainty? Let’s examine some historical data as a reference.

The average length of a bear market is 9.6 months, 289 days.1 The S&P 500 Index crossed into bear market territory on June 13, 2022. If the current bear market follows historical averages, we may be in the early innings. However, if we consider some recent bear markets, the length of the bear market can vary dramatically.2

Bear Market Starts

End (Ultimate Low)

Days to Low

% to Lows from High

3/24/2000

10/10/2002

930

-51%

10/11/2007

3/6/2009

512

-58%

2/19/2020

3/23/2020

33

-35%

Average

492days

Current market low for S&P 500 in 2022 was on 6/16/22 at 3666.77.

Was the recent rally in July an indication of broader, continued gains or merely a bear market rally? It’s yet to be determined. However, there are strategies to help investors get invested and stay invested to take advantage of potential gains.

Dollar cost averaging. While making periodic investments over time does not guarantee performance, it does provide the opportunity to make investments at different price levels – with the goal of acquiring investments at a more favorable average cost.

Stay committed to long-term investing goals. As evidenced from the most recent bear markets, while they can be painful, they do not last forever. History has also shown that bull market returns following bear markets can be significant.

Bull Market Starts

Bull Market Ends

% From Start to End: S&P 500

10/9/2002

10/9/2007

101%

03/9/2009

02/18/2020

398%

03/24/2020

01/03/2022

96%

Avoid trying to time the market. Calling the true market bottom is nearly impossible. According to Crestmont Research, from 2016 -2021, the percentage of up days for the S&P 500 index was 56% – leaving 44% as down days. Through 8/22/2022, the percentage of up and down days for 2022 is effectively equal at 50%.

Avoid decisions purely based on emotion as they can cloud investor behavior. During periods of extreme market volatility, it may be helpful to consider the advice of successful investors. Peter Lynch, legendary manager of the Fidelity Magellan fund: “Long term, the stock market’s a very good place to be. But I could toss a coin now. Is it going to be lower 2 years from now? Higher? I don’t know. The stock market’s been the best place to be over the last 10 years, 30 years, 100 years. But if you need the money in 1 or 2 years, you shouldn’t be buying stocks. In the stock market, the most important organ is the stomach. It’s not the brain.”3

Whether we have seen the market bottom, just experienced a bear market rally or we are only in the early stages of a prolonged bear market, ESI partners with quality sponsors that make a variety of resources available to help clients manage periods of volatility and uncertainty. Whether it’s social medial posts, client educational materials or scheduling calls with asset managers, ESI is happy to assist reps and your clients. Please contact ESI Business Development at 800-344-7437 to discuss investing resources.

Dan Randall, CFP®, CLU, ChFC Vice President – Product Management, Equity Services Inc

1 10 Things You Should Know About Bear Markets, The Hartford, 12/21/21

2 Bear Market Rallies, Forbes, 6/23/2022

3 Lessons from an investing legend, 8/11/2021 Fidelity

Compliance with the Securities Exchange Commission’s (“SEC”) new Marketing Rule (“Rule”) will be required on November 4, 2022. Below are some highlights of what to know about the Rule, and how these changes affect you. Please note that the changes to EFA’s policies and procedures discussed below are not in effect, yet, but will be effective prior to the November 4th deadline.

THE “OLD” RULES

Current SEC Rules[1] consider it to be a violation for any Investment Adviser to publish a “testimonial” concerning the adviser’s advice, analysis or other services. This means that, today, ESI Financial Advisors (“EFA”) and its Investment Adviser Representatives (“IARs”) cannot publish advertisements, on social media or otherwise, with statements such as:

“Hello, I’m John Smith, public school teacher. I’ve worked with Mary Shields at EFA for forty years. She’s always been there for me, and she’s helped me to plan for a more comfortable retirement. You should call her. She can probably help you, too.”

“I’m star quarterback Max Power, and I love my Advisor at EFA, Reed Rothchild. Don’t drop the ball! Call them today and open up an account!”

Notwithstanding this ban on testimonials, referrals of a specific client to an IAR or advisor are generally permitted if the solicitation rules are complied with.[2] Specifically, an Advisor is permitted to pay a cash fee to a solicitor who refers business to them, as long as there is a written agreement with the solicitor and the advisor, the solicitor distributed the advisor’s ADV, and the solicitor provided their own disclosure document (which discussed, among other things, the solicitor’s compensation).[3]

Additionally, as long as the person making the referral did not base it on an individual’s specific investment needs, impersonal referral arrangements are generally not considered to be solicitations by the SEC, and are permitted without complying with the solicitation rules and their disclosure requirements.[4] As a result, people like Dave Ramsey are allowed to have a network of “Endorsed Local Providers” that they refer business to, and you yourself may have similar informal networking arrangements. For example, you may agree with a CPA to send clients to him or her, if the CPA agrees to send clients your way.

THE NEW RULES

In December 2020, the SEC approved amendments to Rule 206(4)-1, which combines new regulatory approaches to advertisements and solicitations. These changes take effect November 4, 2022.

Promoters: The new rules introduce the concept of a “Promoter,” which is a person or company that provides “testimonials” or “endorsements,” whether or not they receive compensation. “Testimonials” are statements by clients of the adviser that solicit others to become clients. “Endorsements” are the same types of statements but are made by non-clients. Promoters that provide testimonials or endorsements include:

Subscription-based referral services – websites or other entities that pair potential investors with local advisors (such as SmartAsset, Ramsey Solutions, or WiserAdviser, for example) to which the advisor pays a fee for the service;

Referral arrangements with other professionals – such as attorneys, CPAs, insurance agents, etc. – that involve cash or non-cash compensation;

Traditional solicitation agreements with other professionals that actively solicit advisory business on your behalf; and

Any other relationship or arrangement that results in the referral of potential investors for advisory-related services.

If you use promoters and enter into arrangements to generate referrals to you, you will need to comply with ESI’s new requirements, described below.

Contract Requirement (Promoter Agreement): EFA is required to have an agreement in place with all Promoters if the amount of compensation (whether cash or non-cash compensation) is more than $1,000. Because it will be unclear whether the value of non-cash arrangements exceed this amount, EFA will require that an agreement be in place for all arrangements using promoters.

Disclosure Requirement: This agreement will require the use of a disclosure form, which will meet the rule’s disclosure requirements. These disclosure requirements include, but are not limited to:

Whether the Promoter is a current client of the adviser;

Whether cash or non-cash compensation is provided for the testimonial, endorsement, or solicitation;

A brief statement of any material conflicts of interest on the part of the Promoter that results from their relationship with the adviser; and

The material terms of any compensation arrangement, including a description of the compensation provided or to be provided, directly or indirectly, to the person for the testimonial or endorsement.

For IARs with existing referral relationships, such as informal networking agreements and cross-referral agreements with other professionals, formal referral arrangements with media personalities, or traditional solicitor relationships, you will be required to execute the new Promoter Agreement. This includes relationships where no cash compensation exchanges hands, but each party agrees to refer clients to the other. Click here for a copy of the new Promoter Agreement.

Sometimes you will act as a solicitor, referring clients to other advisors. For example, when you refer a client to Maple Capital, Brinker or AssetMark, you are acting as a Promoter. In these instances, you will use the agreement and disclosure required by those advisors.

What’s Changing:

Informal networking arrangements, and other formal arrangements where business was referred to you on an impersonal basis, will be subject to new compliance requirements and oversight; and

Advertisements, including social media posts, will be allowed to use testimonials and endorsements, as long as they comply with certain rules. Advertisements on social media can only be provided via an approved business-related website and will be subject to review by the Advertising Guidance Team (“AGT”) prior to posting live on the website.

what’s next?

ESI is working on updating its policies and procedures, as well as various documents impacted by the changes, and anticipates adopting the new regime in conjunction with the November 4, 2022 compliance date. There will be additional communication, particularly regarding implementation of the new Promoter Agreement, as we approach the final compliance date.

QUESTIONS

If you have any questions regarding this notice, please feel free to contact ESI Compliance at 800-344-7437.

[4]See Excellence in Advertising, Ltd., SEC No-Action Letter (December 15, 1986) (opining that it was not solicitation to advertise the financial planners generally, and then invite listeners to contact them for a referral to an investment adviser representative who had paid a fee, where the referrals were based on geography without considering a caller’s individualized needs); Int’l Ass’n for Financial Planning, SEC No-Action Letter (June 1, 1998) (same, but also opining that inquiring about general areas of interest pre-referral did not constitute a solicitation); Nat’l Football League Players Ass’n, SEC No-Action Letter (January 25, 2002)(same, even though referrals were not based on geography).

Feedback is key for us to learn where our strengths are, where there is room for improvement, and how best to move forward with achieving our goals. Please help us by filling out our Annual Sentiment Survey.

Last year ESI sent it’s first Annual Sentiment Survey to registered representatives and administrative staff in the field to get a baseline on how we are doing at a very high level. The survey was designed to assess your experience in working with ESI holistically. Are we meeting your needs? Are we helping grow your business? And most importantly are we helping you, help your clients achieve their financial goals?

Over the past year we have spent time analyzing your responses and implementing changes that we felt would be most impactful. An example of this was the creation of the Partner Experience Group to overhaul our onboarding process and facilitate trainings for experienced producers.

The feedback we received was overwhelmingly positive, but we only heard back from 13% of you.

Be on the lookout for an email with an invitation to complete the survey on Monday September 19th.

Starting Monday September 19th you will be able to connect your @nlgroupmail.com email address with your Redtail CRM system. This connection will allow you to manage your calendar wherever you go, push contacts from Redtail to Outlook, and even send emails from within Redtail so you do not have to switch between screens so often.

With this deeper integration, there is a need for additional protection of your client’s data. Beginning September 15th Redtail will require you set up Multifactor Authentication (MFA) on your account. Adding MFA reduces the risk of a hacker gaining access to your system, stealing client information, and even impersonating you. This is a critical security measure that protects you and your clients.

Enabling the integration is easy, and you can choose to enable just the calendar, just the email feature or both.

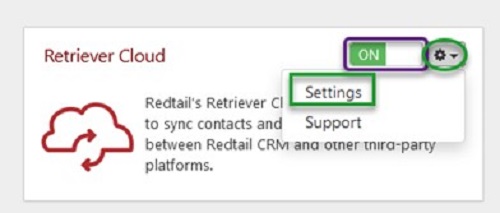

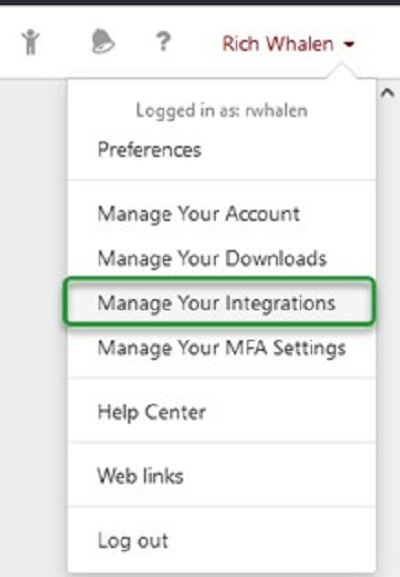

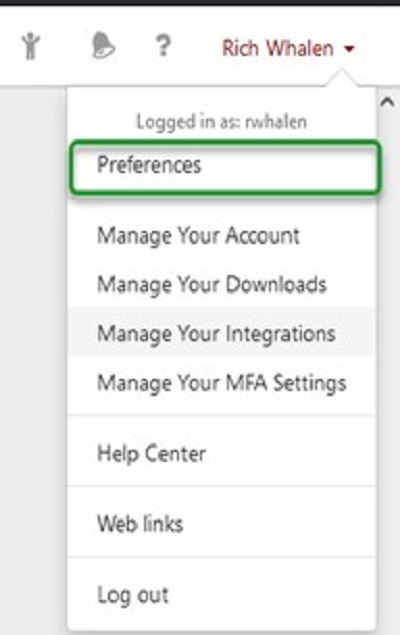

To activate the calendar sync, go to Manage Your Integrations and select Retriever Cloud. Make sure the integration switched to on, then click on the gear icon and select settings.

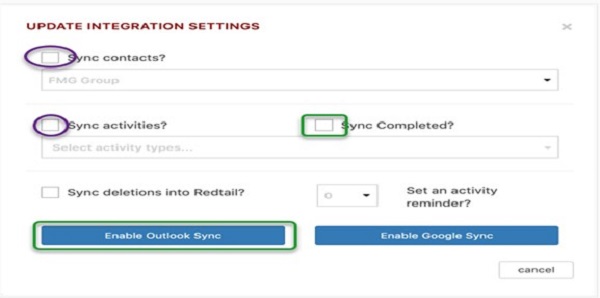

From here you can choose to sync clients, activities (calendar) or both. Be sure to check the sync deletions box if you plan to manage your calendar in Outlook. Finally click on the enable Outlook sync box to enter you agent portal credentials and finalize the connection.

For more information on the cloud retriever feature check out this article from Redtail.

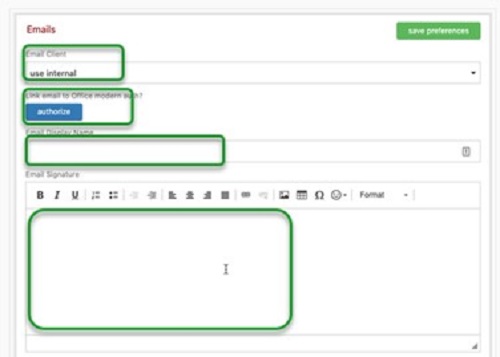

To be able to email from Redtail you need to pull up the preferences menu in Redtail and scroll down until you get to the email section. Change the email client from external to internal, enter you name as you’d like clients to see it and copy your email signature from Outlook. Finally click the authorize button and follow the instructions to connect Outlook.

Don’t worry SmartOffice users. We are going to look into the Outlook-SmartOffice integration capabilities next!

Reverse Stock Split of Certain Touchstone Fund’s Class C Shares

Effective Date – after close of business October 14, 2022

During their August 18th meeting, the Touchstone Board of Trustees approved a Reverse Stock Split for Class C shares of five Touchstone Funds. The Reverse Stock Split will be completed as outlined in the table below after the close of business on or about October 14, 2022 (the “Effective Date”). Shareholders who own Class C shares of these Funds will receive a proportional number of Class C shares as of the Effective Date. The total dollar value of a shareholder’s investment in the Fund will be unchanged and each shareholder will continue to own the same percentage (by value) of the Fund immediately following the Reverse Stock Split as the shareholder did immediately prior to the Reverse Stock Split.

The Reverse Stock Split will not be a taxable event, nor does it have an impact on the Fund’s holdings or its performance. The Board approved the Reverse Stock Split in order to bring the NAV of the Fund’s Class C shares into better alignment with the NAVs of the Fund’s other share classes. For additional information, Touchtone is providing copies of the prospectus supplements related to this corporate action.

This is the first of several Touchstone communications as the operational details for this Reverse Stock Split will be provided in future communications.

The Reverse Stock Split Ratios for the impacted Touchstone Funds are in the table below which are based on the NAV of the Fund’s Class C shares as of August 17, 2022.

TA #

CUSIP

TICKER

SHARE CLASS

TOUCHSTONE FUND NAME

Reverse Stock Split Ratio (old to new)

90

89154X807

TGVCX

C

Growth Opportunities Fund

1 : 0.670946

43

89154X872

TOECX

C

Mid Cap Growth Fund

1 : 0.466797

28

89154X401

TEQCX

C

Non-US ESG Equity Fund

1 : 0.801806

461

89155T839

TSNCX

C

Sands Capital Select Growth Fund

1 : 0.796098

6501

89154Q240

SSCOX

C

Small Company Fund

1 : 0.379048

Should you have any questions, DTCC participant firms are invited to call BNY Mellon Broker Dealer Services at 1-877-332-2371. For any fund direct business or fund related inquiries, please contact Touchstone Shareholder Services at 1-800-543-0407.

Touchstone Growth Opportunities Fund Touchstone Mid Cap Growth Fund Touchstone Non-US ESG Equity Fund Touchstone Small Company Fund (each, a “Fund” and together, the “Funds”)

Supplement dated August 19, 2022 to the current Prospectus, Summary Prospectus, and Statement of Additional Information for the Funds, as may be amended or supplemented from time to time

The following change applies to the current Prospectus, Summary Prospectus, and Statement of Additional Information for Touchstone Growth Opportunities Fund, Touchstone Mid Cap Growth Fund, Touchstone Non-US ESG Equity Fund and Touchstone Small Company Fund (each, a “Fund” and together, the “Funds”).

At a meeting of the Board of Trustees (the “Board”) of Touchstone Strategic Trust (the “Trust”) held on August 18, 2022, Touchstone Advisors, Inc. (“Touchstone”) proposed, and the Board approved, a reverse stock split of the Funds’ issued and outstanding Class C shares (collectively, the “Reverse Stock Split”). The Reverse Stock Split will be completed as outlined in the table below after the close of business on or about October 14, 2022 (the “Effective Date”). As a result of the Reverse Stock Split, for each Class C share of the Funds that a shareholder owns as of the Effective Date, the shareholder will receive a proportional number of Class C shares of the respective Fund with the same aggregate dollar value. Thus, the total dollar value of an investment in a Fund will be unchanged and each shareholder will

continue to own the same percentage (by value) of the Fund immediately following the Reverse Stock Split as the shareholder did immediately prior to the Reverse Stock Split. The Reverse Stock Split will not be a taxable event, nor does it have an impact on a Fund’s holdings or its performance. No changes are contemplated at this time for the other share classes offered by the Funds.

The Reverse Stock Split will be carried out in accordance with a stock split ratio calculated to result in net asset values per share (“NAVs”) that better align the share class prices of the respective Funds. The ratios, which are based on the NAVs of each respective Fund’s Class C shares as of August 17, 2022, are shown in the table below.

Fund

Reverse Stock Split Ratio (Old to New)

Touchstone Growth Opportunities Fund – Class C

1 : 0.670946

Touchstone Mid Cap Growth Fund – Class C

1 : 0.466797

Touchstone Non-US ESG Equity Fund – Class C

1 : 0.801806

Touchstone Small Company Fund – Class C

1 : 0.379048

The Class C shares of each Fund will be offered, sold, and redeemed on a Reverse Stock Split-adjusted basis beginning on the first business day following the Effective Date. Each shareholder’s next account statement after the Reverse Stock Split is completed will reflect the Reverse Stock Split.

Reason for the Class C Shares Reverse Stock Split

The Board approved the Reverse Stock Split in order to bring the NAVs of eachFund’s Class C shares into better alignment with the NAVs of the Fund’s other share classes. The Reverse Stock Split is designed to reduce the variance between the NAVs of Class C shares and the other share classes of each respective Fund. This is intended to reduce marketplace confusion and bring greater uniformity to the ratio of capital gains to the NAVs across the classes of each Fund.

Touchstone Sands Capital Select Growth Fund (the “Fund”)

Supplement dated August 19, 2022 to the current Prospectus, Summary Prospectus, and Statement of Additional Information for the Fund, as may be amended or supplemented from time to time

Notice of Reverse Stock Split of Class C Shares

The following change applies to the current Prospectus, Summary Prospectus, and Statement of Additional Information, each dated January 28, 2022, for Touchstone Sands Capital Select Growth Fund (the “Fund”).

At a meeting of the Board of Trustees (the “Board”) of Touchstone Funds Group Trust (the “Trust”) held on August 18, 2022, Touchstone Advisors, Inc. (“Touchstone”) proposed, and the Board approved, a reverse stock split of the Fund’s issued and outstanding Class C shares (the “Reverse Stock Split”). The Reverse Stock Split will be completed as outlined in the table below after the close of business on or about October 14, 2022 (the “Effective Date”). As a result of the Reverse Stock Split, for the Class C shares of the Fund that a shareholder owns as of the Effective Date, the shareholder will receive a proportional number of Class C shares of the Fund with the same aggregate dollar value. Thus, the total dollar value of an investment in the Fund will be unchanged and each shareholder will continue to own the same percentage (by value) of the Fund immediately following the Reverse Stock Split as the shareholder did immediately prior to the Reverse Stock Split. The Reverse Stock Split will not be a taxable event, nor does it have an impact on the Fund’s holdings or its performance. No changes are contemplated at this time for the other share classes offered by the Fund.

The Reverse Stock Split will be carried out in accordance with a stock split ratio calculated to result in a net asset value per share (“NAV”) that better aligns the share class prices of the Fund. The ratio, which is based on the NAV of the Fund’s Class C shares as of August 17, 2022, is shown in the table below.

Fund

Reverse Stock Split Ratio (Old to New)

Touchstone Sands Capital Select Growth Fund – Class C

1 : 0.796098

The Class C shares of the Fund will be offered, sold, and redeemed on a Reverse Stock Split-adjusted basis beginning on the first business day following the Effective Date. Each shareholder’s next account statement after the Reverse Stock Split is completed will reflect the Reverse Stock Split.

Reason for the Class C Shares Reverse Stock Split

The Board approved the Reverse Stock Split in order to bring the NAV of the Fund’s Class C shares into better alignment with the NAVs of the Fund’s other share classes. The Reverse Stock Split is designed to reduce the variance between the NAVs of the Class C shares and the other share classes of the Fund. This is intended to reduce marketplace confusion and bring greater uniformity to the ratio of capital gains to the NAVs across the classes of the Fund.

Please contact your financial advisor or Touchstone at 800.543.0407 if you have any questions.

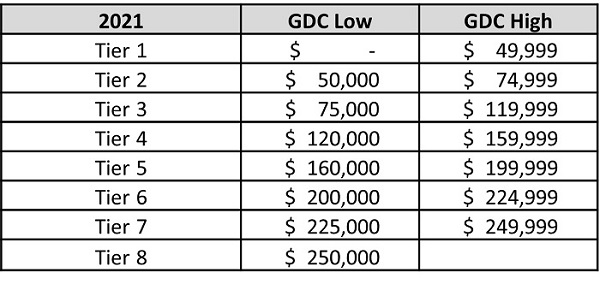

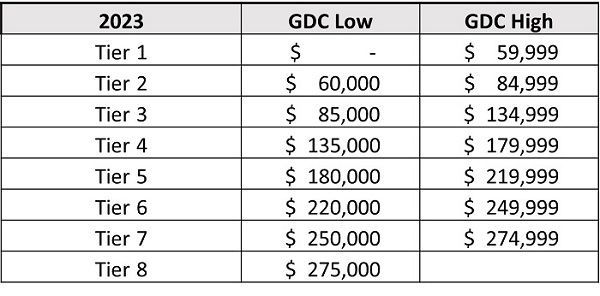

In 2019, ESI restructured our commission grid, creating a total of eight target production bands. This update helped provide achievable goals for our Registered Representatives, maintain best in class payouts, and ensure the revenue necessary to sustain the company’s, product, technology and service offerings.

In alignment with these goals, the Firm will be raising the bar on target production, beginning January 1, 2023. Please consult with your Branch Office Supervisor for your current payouts associated with each tier or view your payouts on the NL Agent Portal. The updated tiers are listed below as well as a screenshot of the the ESI Commission Portal (ACE) location. There are no changes to the EFA Managed Money grids.

Feedback is key for us to learn where our strengths are, where there is room for improvement, and how best to move forward with achieving our goals. Please help us by filling out our Annual Sentiment Survey.

Last year ESI sent it’s first Annual Sentiment Survey to registered representatives and administrative staff in the field to get a baseline on how we are doing at a very high level. The survey was designed to assess your experience in working with ESI holistically. Are we meeting your needs? Are we helping grow your business? And most importantly ae we helping you, help your clients achieve their financial goals?

Over the past year we have spent time analyzing your responses and implementing changes that we felt would be most impactful. An example of this was the creation of the Partner Experience Group to overhaul our onboarding process and facilitate trainings for experienced producers.

The feedback we received was overwhelmingly positive, but we only heard back from 13% of you.

Be on the lookout for an email with an invitation to complete the survey on Monday September 19th.