We’ve made a few updates to the EFA Planning and Consulting program to provide greater clarity, smoother pricing transitions, and more consistent guidance for advisors working with both individuals and business owners. Below is a quick overview of what’s changing and what it means for your practice.

Clarifying Planning vs. Business Consulting

EFA Planning and Consulting remains focused on helping individuals and families with their personal financial planning and investment goals.

For clients who are business owners, it’s perfectly appropriate to incorporate their business interests into the planning process—as long as the discussion connects back to their personal financial picture (retirement, disability planning, education funding, etc.).

If you’re providing consulting that is strictly about the business itself—and not tied to personal planning—those services should be handled as an Outside Business Activity (OBA). This ensures clarity for you, the client, and the firm. As always, OBAs require prior written notice and approval, and securities-related activities must still be conducted through ESI.

The key takeaway:

- Personal planning that considers a client’s business = part of EFA planning

- Stand-alone business consulting = OBA

You can do both simultaneously, as long as each engagement is clearly defined.

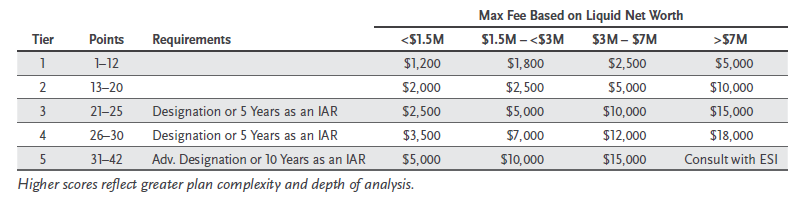

Smoother Fee Tiers in the Pricing Matrix

To reduce large jumps between pricing levels, we’ve added an additional tier to the EFA pricing matrix. This creates more flexibility when structuring planning and consulting fees.

Designation/experience requirements:

- Tier 3–4: Approved designation or 5+ years as an IAR

- Tier 5: Advanced designation or 10+ years as an IAR

As a reminder, total fees are still capped based on client net worth and income. The allowable fee remains the lower of:

- The pricing matrix limit

or - The higher of 1% of net worth or income

Updates to the Plan Complexity Matrix

A few refinements were made to improve consistency:

- “Years to goal” is now “years to retirement”

- A new comment field has been added to explain higher complexity scores when applicable

These adjustments are designed to make scoring more intuitive and easier to document.

Helpful Resources

For more details and step-by-step guidance, refer to:

TC8765570(0226)1